Happy Wednesday!

I’m not a fan of annuities.

If you’ve been following my writing for any length of time, this will come as no surprise to you.

But not all annuities are junk.

Just most of them.

To wit…

Let’s begin with this 2019 article I wrote for Seeking Alpha:

If you didn’t already know about my distaste for annuities, the article above makes it pretty clear.

But I’d encourage you to read the 50 comments on my article too.

They range from “I agree with every word of your article” to calling my article “Very misleading and inaccurate…”

I can’t help but wonder which of these commenters’ rely on the sale of annuities to support themselves and their business.

I have my suspicions. Maybe you will too.

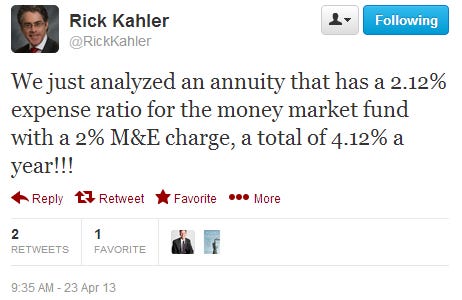

Here’s a 2013 tweet from advisor Rick Kahler:

I’ve run into these levels of egregious annuity fees myself. And much more recently than 2013.

Here’s another 2013 article from Financial Advisor:

Here’s what caught my attention in the article:

“We’re getting more than 2 percentage points of fees from the assets that are part of our annuity business,” Mark Grier, Prudential’s vice chairman, said at a Citigroup Inc. financial-services conference in Boston today. “In your businesses, you probably would dance in the street over 40 or 50 or 60 basis points.” A basis point is 0.01 percentage point.

Or this Forbes article from another fee-only, fiduciary advisor like myself:

How about this small but very important point highlighted by fellow advisor Allan Roth in his August 2023 article:

Every FIA [Fixed Indexed Annuity] contract I’ve reviewed has the unilateral right of the insurance company to change the terms of the contract, such as lowering that 12% cap. Pfau agreed that insurance companies have that right. I asked Pfau how low those caps could go, and he responded, “As low as 1-2%.” I’ve seen 0.25%, meaning the contract owner would get between 0% and 0.25% annually. This right of the insurance company to slash returns was not mentioned in Pfau’s paper.

And if the annuities themselves weren’t already problematic, there’s a lot of salespeople masquerading as financial professionals hoping you’re their next fat commission check from an annuity sale.

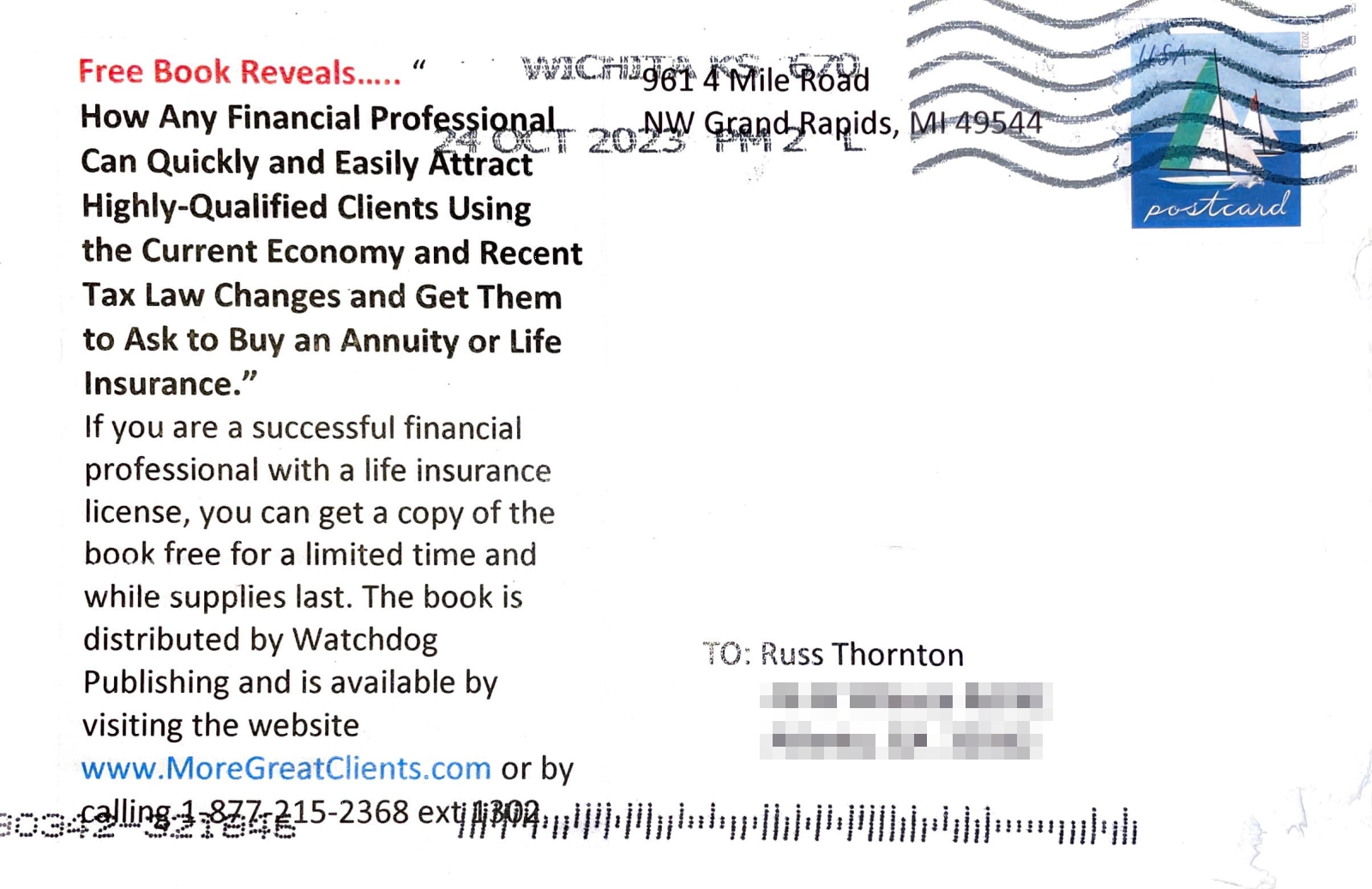

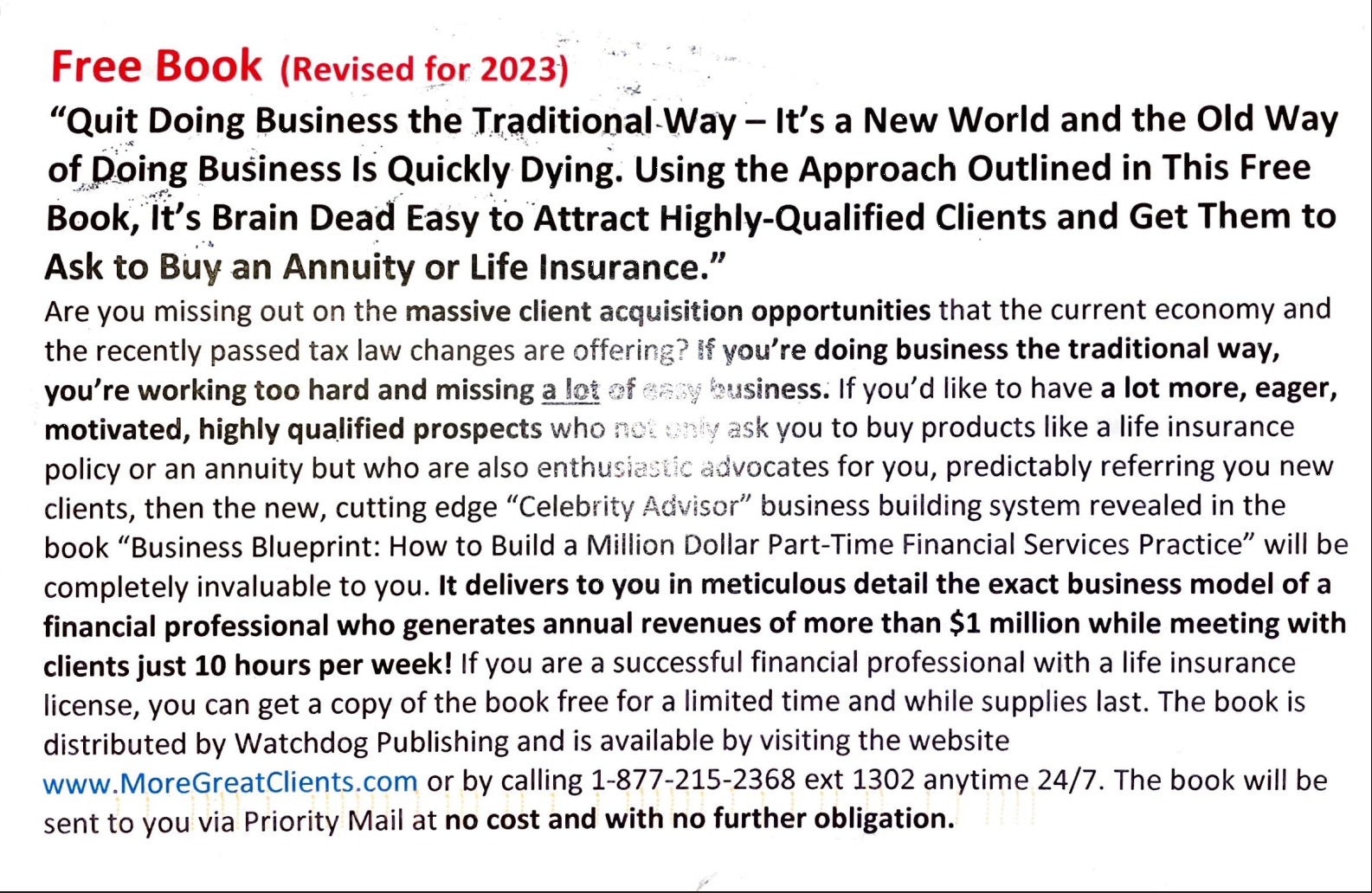

I got this postcard in the mail just last week:

Here’s the other side of the postcard:

Unfortunately, there are all sorts of these “sales systems” out there, and annuities and certain types of life insurance seem to be their weapons of choice.

You know those “educational” steak dinners I wrote about recently?

They often serve an annuity sales pitch for dessert.

Now, having gotten that off my chest, I’ll admit I have a few annuities among my clients.

In all cases, these are the result of what I consider an annuity “rescue attempt.”

Many times, annuities are sold to people inside their IRA accounts. This is a problem on its own, but when there aren’t prohibitive fees to do so, we’ll terminate the annuity and put the funds into a regular IRA account.

But when an annuity is held outside an IRA account, you can’t just liquidate it without incurring income taxes on any growth and earnings on the original money used to purchase the annuity.

In these non-IRA rescue attempts, we’ll look for a less costly, more flexible replacement annuity to preserve the tax deferral and avoid a big tax bill.

Which is how and why I have a couple of clients with annuities right now.

Other times it’s a long, slow rescue attempt.

I’ve had clients who not only have an expensive annuity, but the person who sold it to them must have been paid quite a healthy up-front commission.

I only know this because there are “surrender fees” that last for years and years. This means the client can’t take the money out and move to another less expensive annuity without being charged a percentage of the annuity’s value on the way out the door.

Insurance companies use these surrender fees to unofficially “lock” your funds inside the annuity while they capture fees over time to make up for the commission paid to the salesperson. Or to recoup the “bonus premium” you received when you were sold the annuity.

In this situation, we move a little each year to another less costly, more flexible annuity without triggering the surrender charges.

If I haven’t convinced you to be wary of annuities, at least consider yourself forewarned…

But - and this is a BIG but - not all annuities are bad.

Some have their place.

Not all annuities are the variable or fixed indexed type, which is where high fees and complicated contract provisions seem most common.

There are also:

Click each of the links above to learn more. They’re pretty interesting and have unique use cases.

And maybe - just maybe - one of these makes sense in your situation.

Or maybe not.

Just like virtually every other financial (and life) decision, annuities involve trade-offs.

Please just make sure you fully understand these trade-offs before doing anything with your hard-earned money.

Especially if it involves an annuity or any type of life insurance other than a term policy.

Reach out to me if you have questions about this or would like to discuss any of this further.

Clearly, I have an opinion. 😉

I’m glad you’re here. And I’m grateful to have you as a reader.

Interested in working together?

My name is Russ. I’ve been delivering personal financial advice to clients and families for more than 30 years and have helped countless women get ready for retirement, care for their families, protect their wealth—and most importantly, live great lives.

linkedin

Have questions or want to discuss anything?

Please feel welcome to get in touch.

Want to read and learn more?

Check out my blog and subscribe to my free weekly newsletter.