Today, I’d like to dig a little deeper into this topic and attempt to show you the impact a brokerage account can potentially have on your after-tax retirement income…

First, let me introduce you to Jane.

She’s 62 years old, has just retired, and has $2,000,000 in accumulated investments to help provide her retirement income.

To keep things simple, I’m not including any Social Security or other income sources. And we’re not including any additional assets in Jane’s plan.

And we’re assuming Jane will live to age 95.

She lives in Georgia.

I’m going to isolate the impact to Jane’s sustainable retirement income based on whether her portfolio is all in an IRA or all in a taxable brokerage account.

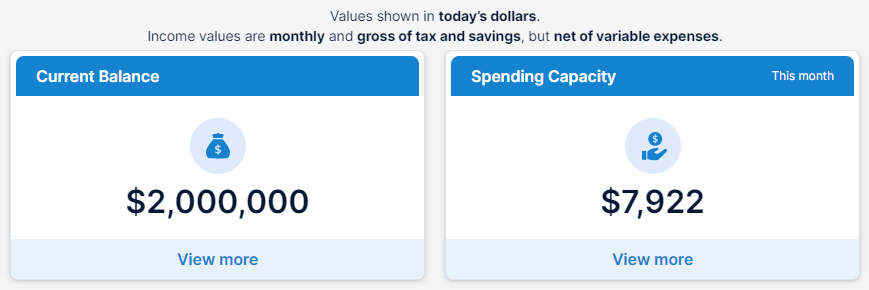

Let’s start with Jane’s entire $2 million portfolio in her IRA:

As you can see above, her portfolio value is $2 million and her starting monthly pre-tax income is $7,922.

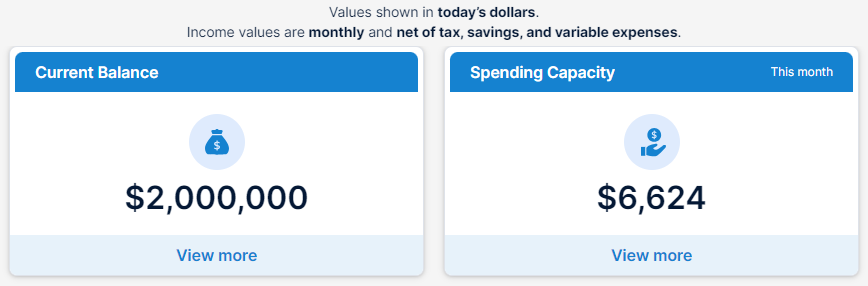

But what if we look at her after-tax monthly income?

Based on the difference between Jane’s pre-tax and after-tax monthly income amount, the analysis assumes she’ll have to pay approximately $1,298 in taxes on her $7,922 gross retirement income.

She’ll get to spend $6,624 in her first month of retirement.

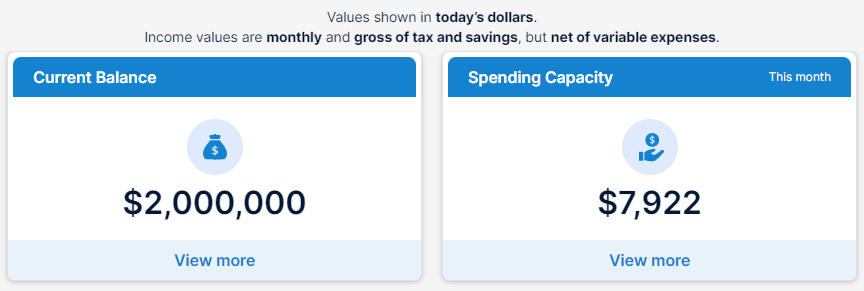

Now, let’s look at the same scenario, but let’s assume Jane’s entire $2 million portfolio is in a taxable brokerage account:

As expected, same pre-tax income as with the IRA example above.

But it gets more interesting when we compare the after-tax income amounts:

Note: I’m assuming the $2 million taxable brokerage account has a cost basis of $1.5 million. In other words, I’m assuming there are already $500,000 in unrealized capital gains in Jane’s portfolio.

There’s only a difference of approximately $128 between the pre- and after-tax income amounts when we assume Jane’s entire portfolio is in a taxable brokerage account.

And while it’s unlikely - though not unheard of - to have all of your long-term investments in either an IRA or a brokerage account, I just wanted to illustrate the potential impact one “tax bucket” can have relative to another.

Let’s look at it from another perspective.

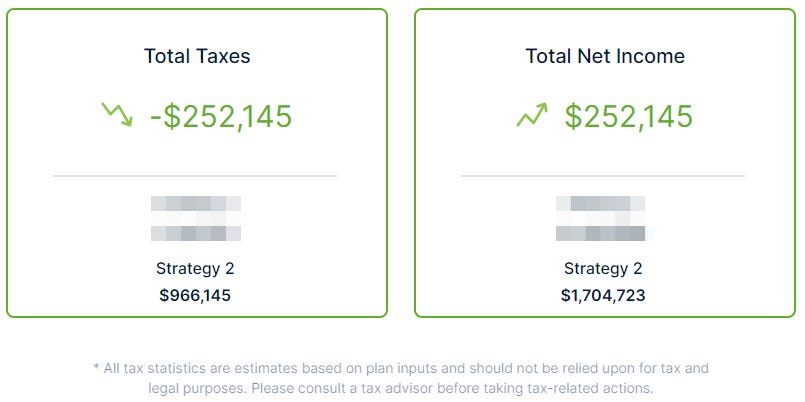

Here’s the IRA scenario:

The numbers above attempt to calculate the total lifetime taxes that will be owed as well as the total lifetime after-tax income Jane could expect.

Here are the same numbers for the taxable brokerage account:

Note: Please ignore the numbers in green in the boxes above as they’re illustrating something unrelated to our discussion today.

As you can see, the taxable brokerage account scenario results in approximately $537,000 less tax paid over Jane’s lifetime. And she captures this entire tax savings in additional after-tax retirement income.

I realized it might be more helpful to show you the potential impact of a brokerage account rather than just telling you.

A few important notes and assumptions:

As with all things financial, it’s best to strike a balance.

Save into your 401k AND start investing in a brokerage account once you can afford to do so.

And if you’re close to retirement or already retired, make the best plan with what you have.

And be sure to do some tax planning along the way.

Interested in working together? Schedule a meeting!

I’m glad you’re here. And I’m grateful to have you as a reader.

Interested in working together?

My name is Russ. I’ve been delivering personal financial advice to clients and families for more than 30 years and have helped countless women get ready for retirement, care for their families, protect their wealth—and most importantly, live great lives.

linkedin

Have questions or want to discuss anything?

Please feel welcome to get in touch.

Want to read and learn more?

Check out my blog and subscribe to my free weekly newsletter.